← Back

American Yttrium? The Overlooked Chokepoint for Jet Engines and Semiconductors

Yttrium is a small-volume metal inside advanced jet-engine coatings and semiconductor manufacturing equipment. Its repricing exposed a deeper Western supply problem.

Yttrium was not the metal that inspired us to set out on this journey.

American Terbium's focus since inception has been on the heavies, dysprosium and terbium in particular, as the name might give away. After the latest yttrium rally, a few of our investors asked whether we should change the company name to American Yttrium. It has a nice ring to it, though I fear if we change the name every time a particular rare earth price pops, our stationery printer might end up with a controlling interest. Still, I bought the domain, just in case.

Yttrium was never a central target of our geologic model. It was present in the assays and in technical reports, but it was not what we were organizing the company around.

Then the price exploded.

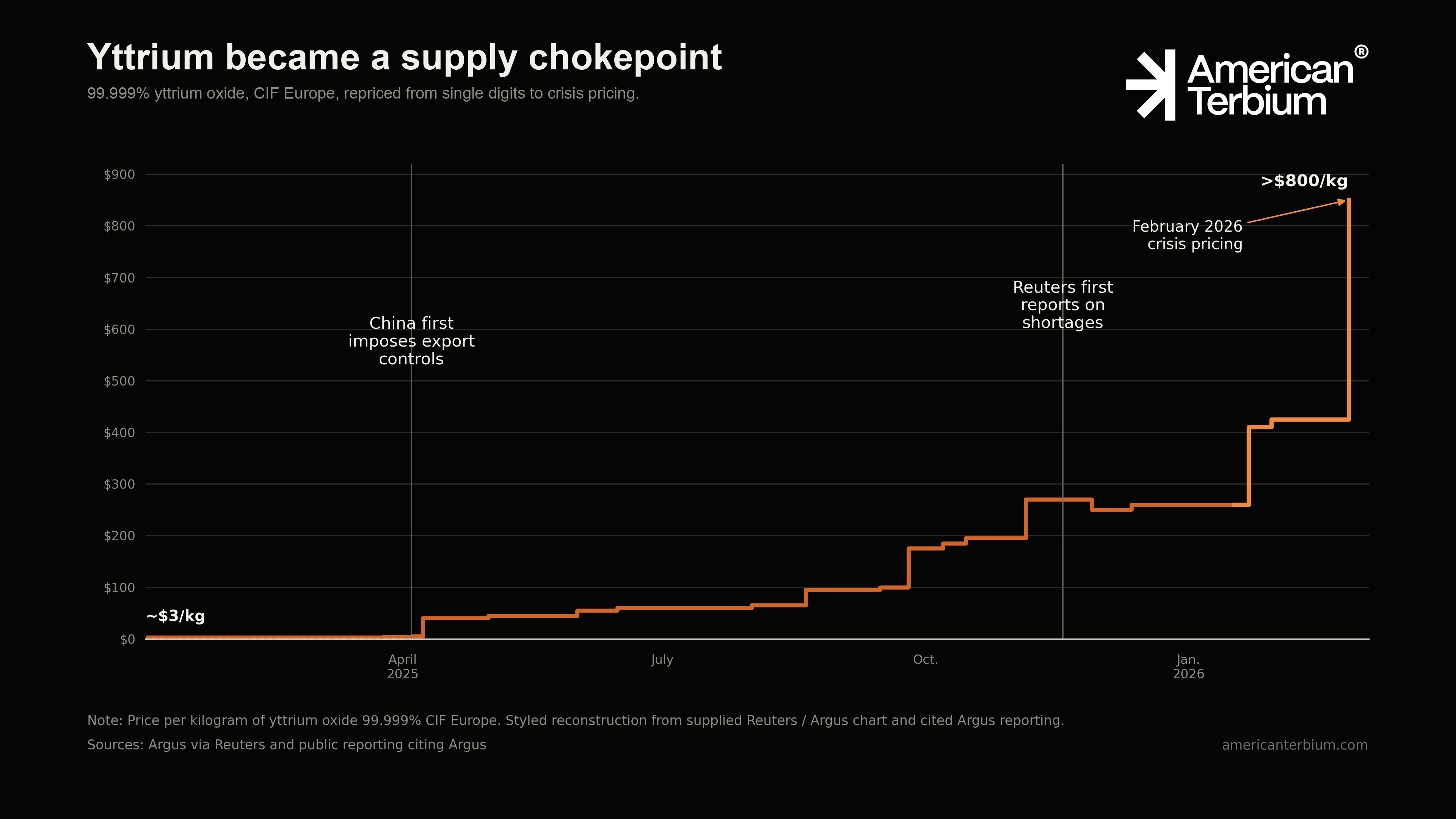

In 2025, USGS put the average 99.999% Y2O3 price at $9/kg FOB China. Reuters later reported European yttrium oxide at $270/kg in November, up 4,400% from January. By late February 2026, quoted prices outside China had printed above $800/kg.

I am not going to pretend those numbers are the same type of price. FOB China annual averages, European CIF spot, and thin-market crisis prints should not be conflated. A momentary panic-driven spot price is not the basis for a business plan. But clearly disregarding it would be a mistake.

When a metal moves like that due to an export-control shock, the price is telling you that the old market did not carry enough insurance for supply security.

Price Was a Warning

On April 4, 2025, China placed export controls on yttrium metal, yttrium-bearing alloys, targets, yttrium oxide, and yttrium-bearing compounds. Essentially the entire product catalog.

Reuters later reported that U.S.-bound shipments fell to 17 tonnes in the eight months after the controls, from 333 tonnes in the eight months before. A 60-ton March 2026 yttrium oxide shipment to the U.S. showed that some licensing was moving again. Reuters also reported that U.S.-bound yttrium oxide exports over the prior 12 months were still down 75% year over year.

This matters more than a single rally.

Some analysts, like Adamas Intelligence, have warned that European ask prices can overstate the amount of material actually trading, which is fair.

The uncomfortable part remains: a China domestic price and a Western delivered price can have a vast spread when a buyer is willing to pay whatever it costs to guarantee delivery of the raw materials they need to meet multibillion-dollar defense contracts. That is what price inelasticity looks like.

Chart note: price per kilogram of 99.999% yttrium oxide, CIF Europe. Source: Argus.

Where yttrium is a critical dependency.

Yttrium is easy to miss because its applications are somewhat niche.

Unlike dysprosium or terbium, yttrium is not a high-temperature NdFeB story. It sits in thermal barrier coatings for F-35 jet engines and power turbines, ceramics, phosphors, fiber optics, optical glass, semiconductor manufacturing equipment, and YAG crystals used in the most powerful lasers. While substitutes exist for some applications, they are less effective, and for most advanced weapons systems, lasers, and phosphors where there is little margin for error they cannot be substituted.

The tonnages are relatively small and on the surface unimpressive. But this unique metal sits quietly inside the most advanced stealth fighter jets and multibillion-dollar semiconductor production lines.

The Lost Basin Discovery

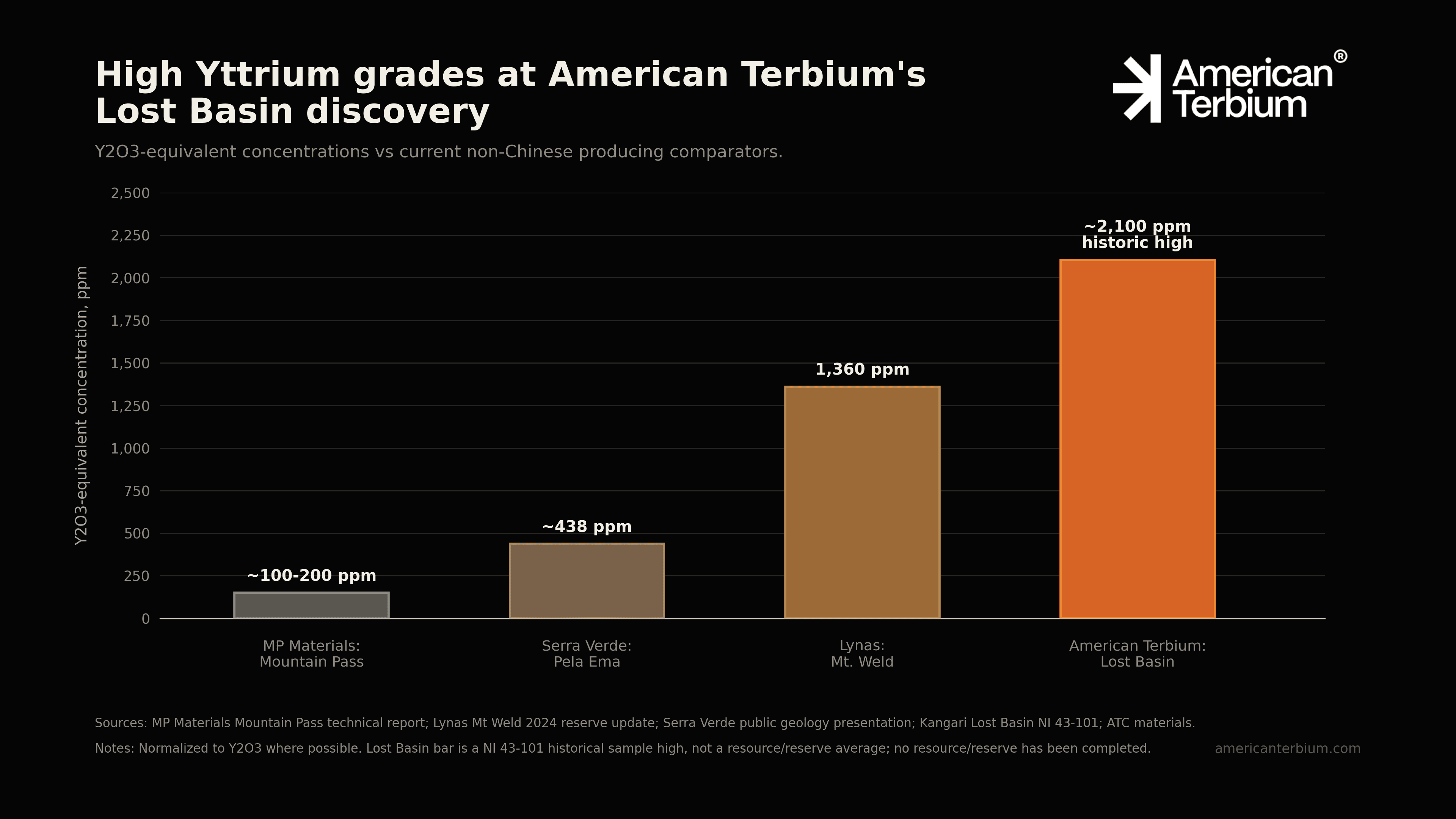

Lost Basin was exciting before the yttrium price moved because the rare earth basket was unusually heavy. Dysprosium, terbium, and yttrium are enriched together at surface, in a deposit style and material that has shown encouraging leach behavior.

With surface highlights of 6,302 ppm TREO from our work there, dysprosium at 221.5 ppm, and terbium at 35.3 ppm, this already stands as one of the single highest grading occurrences of heavy rare earths ever taken from a sedimentary deposit. But yttrium intensity is the real story, with samples as high as 1,671 ppm Y, or roughly 2,122 ppm Y2O3-equivalent using the standard conversion.

Chart note: comparison uses Y2O3-equivalent concentrations where possible. Lost Basin is shown as a historical sample high, not a resource or reserve average.

If the Dy-Tb-Y enrichment proves consistent and laterally extensive across strike, Lost Basin is not just a good sample story. It is a drill-ready project with billions of dollars of exploration potential. But this work remains ahead of us.

That is the version of the story we can confidently claim: a serious North American Dy-Tb-Y story that now warrants serious follow-up work.

Process Before Promotion

The more interesting part is what Lost Basin did to our process thinking.

Our leachability work did more than support a geological model. It forced a practical question: can the heavy fraction, including yttrium, be recovered selectively enough, cleanly enough, and early enough to matter commercially?

I am not going to turn a public newsroom article into a disclosure of our processing technologies, but Lost Basin has been a technical learning ground for us for this new rare earth deposit type.

That work helped give birth to the provisional patent portfolio we filed in April 2026. The portfolio covers pre-treatment, leaching, downstream recovery, process timing, and reagent recovery at a high level. The family most relevant here is YHREE, our provisional around selective yttrium and heavy rare-earth recovery.

The filings do not yet prove commerciality, but they do show where the technical questions have led us: toward the potential selective recovery of the most critical part of the basket.

The Work Ahead

The price chart that got everyone's attention does not answer the exploration question we still have, but it does magnify the upside potential.

Our job is to turn the grades we have found, and the leachability, into a resource and a path to production. That means drilling, bulk sampling, repeatable metallurgical data, and eventual qualification with midstream partners and end users who need dependable non-Chinese material.

If Lost Basin's Dy-Tb-Y profile can be translated into a resource and a partnerable heavy rare earth leach concentrate, the market has started to price a problem we were already working on.

Where This Lands American Terbium

I still see the same strategy, only with a brighter yttrium-colored light on it. To secure the metals our country needs, as always, we must create value in the rocks.

Sources: USGS Yttrium Mineral Commodity Summary 2026, MOFCOM Announcement No. 18 of 2025, Reuters via The Business Standard, Reuters via Taipei Times, Adamas Intelligence.

Thumbnail credit: "The small blue yonder" by Angel Yanguas-Gil, Jeffrey W. Elam, and John N. Hryn. Yttrium oxide crystals activated by atomic layer deposition. Cropped for layout. Licensed under CC BY-NC-SA 2.0.

American Terbium Corp. Appoints Michael Pochna to Its Advisory Board

A piece explaining how tailings retreatment could reduce the path to first production to about 12 months instead of 7–15 years.

American Terbium Announces Company Name Change and Dy-Tb Focus

A piece explaining how tailings retreatment could reduce the path to first production to about 12 months instead of 7–15 years.

NASM Announces New Rare Earth Deposit Model Across North America

A piece explaining how tailings retreatment could reduce the path to first production to about 12 months instead of 7–15 years.

[ Partner with Us ]

American Terbium is developing a modular direct-leach platform to recover critical heavy rare earths—dysprosium, terbium and yttrium—from overlooked U.S. mine tailings and waste rock. Submit an inquiry to discuss investment, offtake or strategic partnerships.

American Terbium Corp. • Delaware Corporation • Founded 2020

Investor Inquiry

Offtake